Article: Use a CD Ladder to save more

Use a CD Ladder to save more, faster, without sacrificing financial flexibility

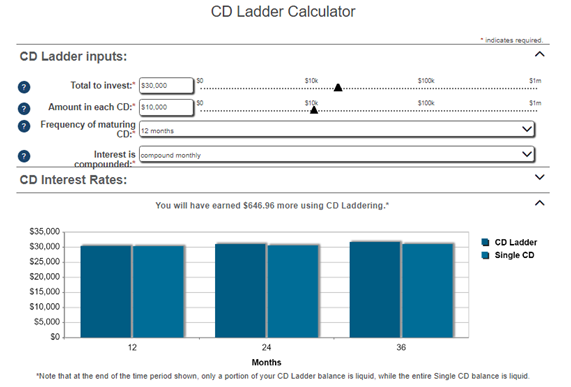

If you're looking for a savings strategy that lets you earn better savings rates – and doesn’t lock up your cash for years at a time – consider building an Advantis CD Ladder using Personal, Business, or IRA CDs.

What is a CD Ladder, and why should you build one?

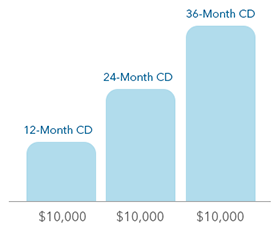

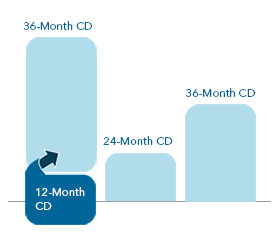

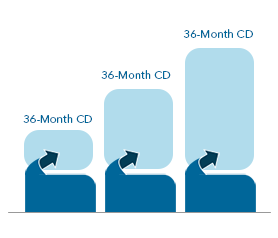

When you build a CD Ladder, you open several High-Growth Certificates of Deposit (CDs), all with different maturity dates. One is, initially, shorter-term, while the others are longer-term. Combined, they become a powerful savings tool called a CD Ladder.

Your CD Ladder lets you make the most of short-term and long-term CDs, eventually creating a self-sustaining cycle of savings returns.

|

|

|

| Short-term CD Shorter terms allow you to access your savings with more frequency, but you can’t maximize interest. |

Long-term CD |

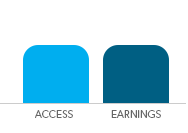

CD Ladder: Best of Both A CD Ladder offers long-term earning power, plus frequent access to a portion of your savings. |

Swipe